Page 74 - Internal Auditing Standards

P. 74

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

5.10 Manual versus Automated Controls

For most entities, the system of internal control will consist of a mixture of manual and automated controls.

The risks and benefits associated with the different types of control are outlined below.

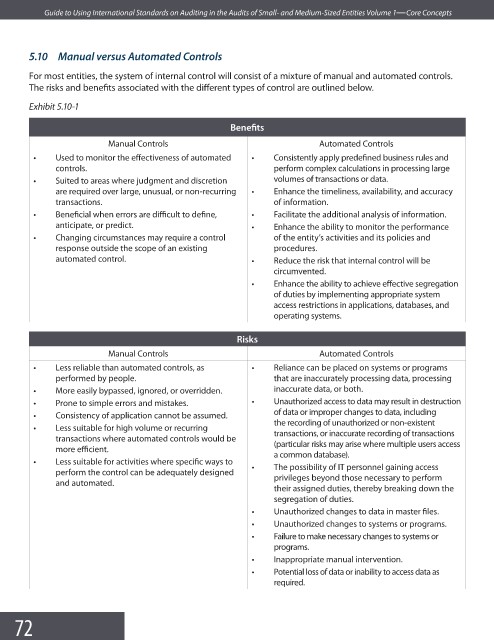

Exhibit 5.10-1

Benefi ts

Manual Controls Automated Controls

• Used to monitor the effectiveness of automated • Consistently apply predefined business rules and

controls. perform complex calculations in processing large

• Suited to areas where judgment and discretion volumes of transactions or data.

are required over large, unusual, or non-recurring • Enhance the timeliness, availability, and accuracy

transactions. of information.

• Beneficial when errors are diffi cult to defi ne, • Facilitate the additional analysis of information.

anticipate, or predict. • Enhance the ability to monitor the performance

• Changing circumstances may require a control of the entity’s activities and its policies and

response outside the scope of an existing procedures.

automated control. • Reduce the risk that internal control will be

circumvented.

• Enhance the ability to achieve eff ective segregation

of duties by implementing appropriate system

access restrictions in applications, databases, and

operating systems.

Risks

Manual Controls Automated Controls

• Less reliable than automated controls, as • Reliance can be placed on systems or programs

performed by people. that are inaccurately processing data, processing

• More easily bypassed, ignored, or overridden. inaccurate data, or both.

• Prone to simple errors and mistakes. • Unauthorized access to data may result in destruction

of data or improper changes to data, including

• Consistency of application cannot be assumed.

the recording of unauthorized or non-existent

• Less suitable for high volume or recurring

transactions where automated controls would be transactions, or inaccurate recording of transactions

(particular risks may arise where multiple users access

more effi cient.

a common database).

• Less suitable for activities where specific ways to

perform the control can be adequately designed • The possibility of IT personnel gaining access

and automated. privileges beyond those necessary to perform

their assigned duties, thereby breaking down the

segregation of duties.

• Unauthorized changes to data in master fi les.

• Unauthorized changes to systems or programs.

• Failure to make necessary changes to systems or

programs.

• Inappropriate manual intervention.

• Potential loss of data or inability to access data as

required.

72