Page 76 - Internal Auditing Standards

P. 76

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

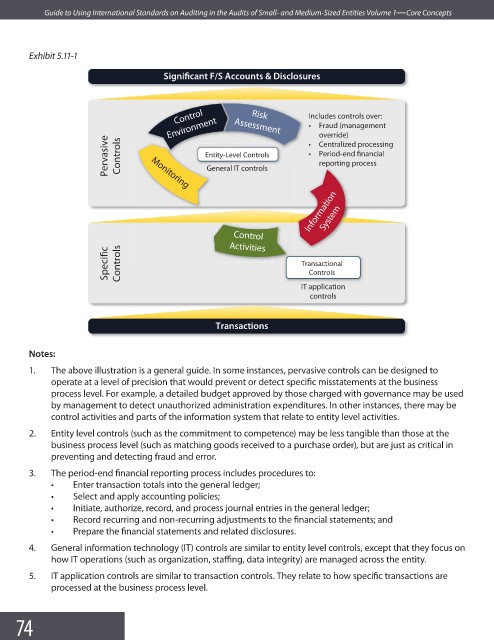

Exhibit 5.11-1

Significant F/S Accounts & Disclosures

Control

Risk

Environment Assessment Includes controls over:

t Fraud (management

override)

Pervasive Controls Monitoring Entit y e -Leve l c Contro l l l s s t Centralized processing

t Period-end financial

Entity-Level Controls

reporting process

p

g

l

l

n

r

a

t

n

t

o

r

I

I

T

o

T

General IT controls

Ge

G

Information

System

Control

Activities

Specific Controls Transactional

Controls

IT application

controls

Transactions

Notes:

1. The above illustration is a general guide. In some instances, pervasive controls can be designed to

operate at a level of precision that would prevent or detect specific misstatements at the business

process level. For example, a detailed budget approved by those charged with governance may be used

by management to detect unauthorized administration expenditures. In other instances, there may be

control activities and parts of the information system that relate to entity level activities.

2. Entity level controls (such as the commitment to competence) may be less tangible than those at the

business process level (such as matching goods received to a purchase order), but are just as critical in

preventing and detecting fraud and error.

3. The period-end financial reporting process includes procedures to:

• Enter transaction totals into the general ledger;

• Select and apply accounting policies;

• Initiate, authorize, record, and process journal entries in the general ledger;

• Record recurring and non-recurring adjustments to the financial statements; and

• Prepare the financial statements and related disclosures.

4. General information technology (IT) controls are similar to entity level controls, except that they focus on

how IT operations (such as organization, staffing, data integrity) are managed across the entity.

5. IT application controls are similar to transaction controls. They relate to how specific transactions are

processed at the business process level.

74