Page 79 - Internal Auditing Standards

P. 79

6. Financial Statement Assertions

Chapter Content Relevant ISAs

Use of management’s assertions in auditing. 315

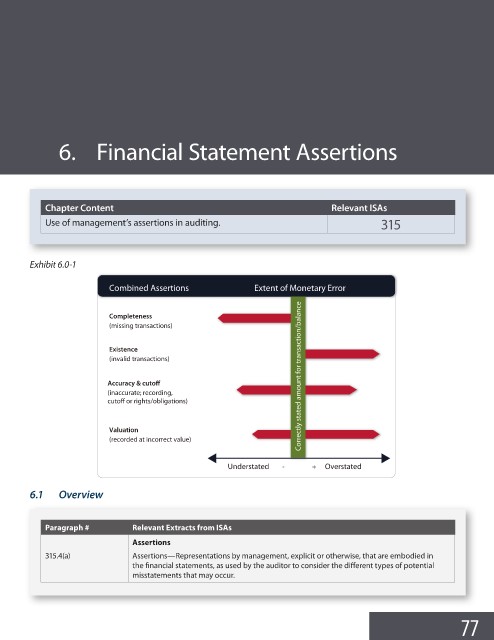

Exhibit 6.0-1

Combined Assertions Extent of Monetary Error

Correctly stated amount for transaction/balance

Completeness

(missing transactions)

Existence

(invalid transactions)

Accuracy & cutoff

(inaccurate; recording,

cutoff or rights/obligations)

Valuation

(recorded at incorrect value)

Understated Overstated

+

-

6.1 Overview

Paragraph # Relevant Extracts from ISAs

Assertions

315.4(a) Assertions—Representations by management, explicit or otherwise, that are embodied in

the financial statements, as used by the auditor to consider the different types of potential

misstatements that may occur.

77