Page 80 - Internal Auditing Standards

P. 80

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

When management makes a representation to the auditors such as “the financial statements as a whole

are presented fairly in accordance with the applicable financial reporting framework,” it actually contains a

number of embedded assertions.

These embedded assertions (by management) relate to the recognition, measurement, presentation, and

disclosure of the various elements (amounts and disclosures) in the fi nancial statements.

Examples of management’s assertions include:

• All the assets in the financial statements exist;

• All sales transactions have been recorded in the appropriate period;

• Inventories are stated at appropriate values;

• Payables represent proper obligations of the entity;

• All recorded transactions occurred in the period under review; and

• All amounts are properly presented and disclosed in the fi nancial statements.

These assertions are often summarized by a single word such as completeness, existence, occurrence,

accuracy, valuation, et al. For example, management may assert to the auditor that the sales balance in the

accounting records contains all the sales transactions (completeness assertion), the transactions took place

and are valid (occurrence assertion), and transactions have been properly recorded in the accounting records

and in the appropriate accounting period (accuracy and cutoff assertion).

6.2 Description of Assertions

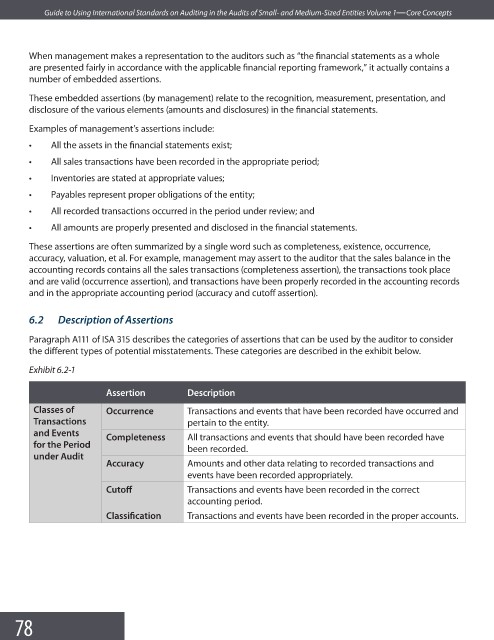

Paragraph A111 of ISA 315 describes the categories of assertions that can be used by the auditor to consider

the different types of potential misstatements. These categories are described in the exhibit below.

Exhibit 6.2-1

Assertion Description

Classes of Occurrence Transactions and events that have been recorded have occurred and

Transactions pertain to the entity.

and Events

Completeness All transactions and events that should have been recorded have

for the Period

been recorded.

under Audit

Accuracy Amounts and other data relating to recorded transactions and

events have been recorded appropriately.

Cutoff Transactions and events have been recorded in the correct

accounting period.

Classifi cation Transactions and events have been recorded in the proper accounts.

78