Page 81 - Internal Auditing Standards

P. 81

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

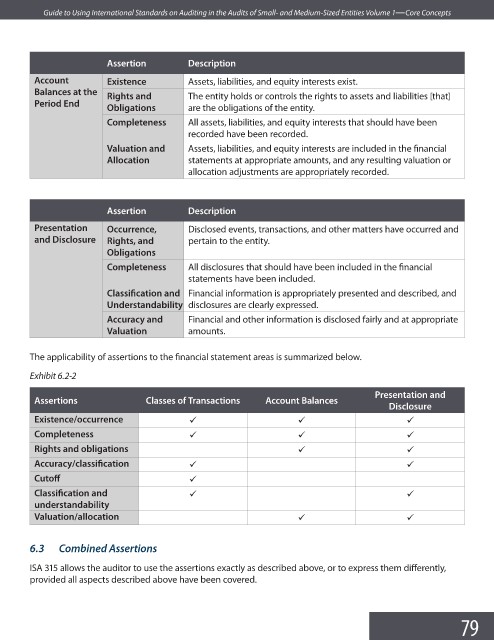

Assertion Description

Account Existence Assets, liabilities, and equity interests exist.

Balances at the Rights and The entity holds or controls the rights to assets and liabilities [that]

Period End

Obligations are the obligations of the entity.

Completeness All assets, liabilities, and equity interests that should have been

recorded have been recorded.

Valuation and Assets, liabilities, and equity interests are included in the fi nancial

Allocation statements at appropriate amounts, and any resulting valuation or

allocation adjustments are appropriately recorded.

Assertion Description

Presentation Occurrence, Disclosed events, transactions, and other matters have occurred and

and Disclosure Rights, and pertain to the entity.

Obligations

Completeness All disclosures that should have been included in the fi nancial

statements have been included.

Classifi cation and Financial information is appropriately presented and described, and

Understandability disclosures are clearly expressed.

Accuracy and Financial and other information is disclosed fairly and at appropriate

Valuation amounts.

The applicability of assertions to the financial statement areas is summarized below.

Exhibit 6.2-2

Presentation and

Assertions Classes of Transactions Account Balances

Disclosure

Existence/occurrence 9 9 9

Completeness 9 9 9

Rights and obligations 9 9

Accuracy/classifi cation 9 9

Cutoff 9

Classifi cation and 9 9

understandability

Valuation/allocation 9 9

6.3 Combined Assertions

ISA 315 allows the auditor to use the assertions exactly as described above, or to express them diff erently,

provided all aspects described above have been covered.

79