Page 30 - Managerial Accounting-MGT 145

P. 30

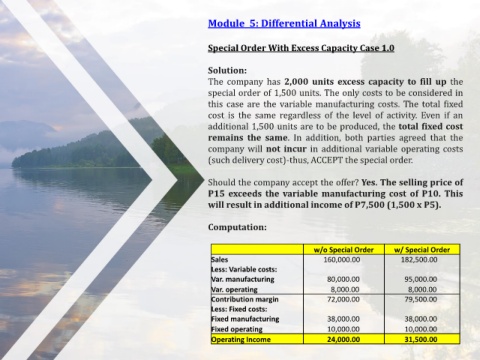

Module 5: Differential Analysis

Special Order With Excess Capacity Case 1.0

Solution:

The company has 2,000 units excess capacity to fill up the

special order of 1,500 units. The only costs to be considered in

this case are the variable manufacturing costs. The total fixed

cost is the same regardless of the level of activity. Even if an

additional 1,500 units are to be produced, the total fixed cost

remains the same. In addition, both parties agreed that the

company will not incur in additional variable operating costs

(such delivery cost)-thus, ACCEPT the special order.

Should the company accept the offer? Yes. The selling price of

P15 exceeds the variable manufacturing cost of P10. This

will result in additional income of P7,500 (1,500 x P5).

Computation:

w/o Special Order w/ Special Order

Sales 160,000.00 182,500.00

Less: Variable costs:

Var. manufacturing 80,000.00 95,000.00

Var. operating 8,000.00 8,000.00

Contribution margin 72,000.00 79,500.00

Less: Fixed costs:

Fixed manufacturing 38,000.00 38,000.00

Fixed operating 10,000.00 10,000.00

Operating Income 24,000.00 31,500.00