Page 32 - Managerial Accounting-MGT 145

P. 32

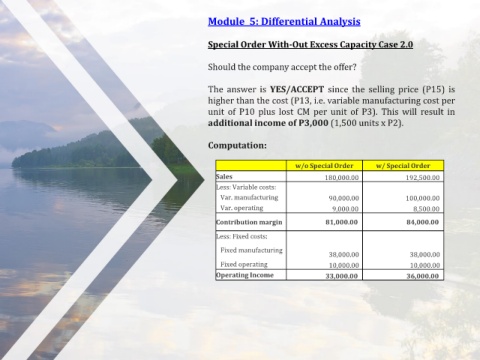

Module 5: Differential Analysis

Special Order With-Out Excess Capacity Case 2.0

Should the company accept the offer?

The answer is YES/ACCEPT since the selling price (P15) is

higher than the cost (P13, i.e. variable manufacturing cost per

unit of P10 plus lost CM per unit of P3). This will result in

additional income of P3,000 (1,500 units x P2).

Computation:

w/o Special Order w/ Special Order

Sales 180,000.00 192,500.00

Less: Variable costs:

Var. manufacturing 90,000.00 100,000.00

Var. operating 9,000.00 8,500.00

Contribution margin 81,000.00 84,000.00

Less: Fixed costs:

Fixed manufacturing

38,000.00 38,000.00

Fixed operating 10,000.00 10,000.00

Operating Income 33,000.00 36,000.00