Page 36 - FINAL CFA II SLIDES JUNE 2019 DAY 10

P. 36

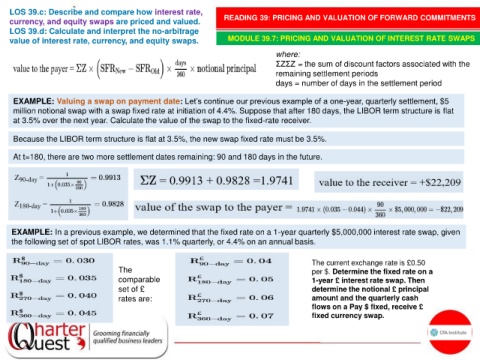

LOS 39.c: Describe and compare how interest rate,

currency, and equity swaps are priced and valued. READING 39: PRICING AND VALUATION OF FORWARD COMMITMENTS

LOS 39.d: Calculate and interpret the no-arbitrage

value of interest rate, currency, and equity swaps. MODULE 39.7: PRICING AND VALUATION OF INTEREST RATE SWAPS

where:

ΣZΣZ = the sum of discount factors associated with the

remaining settlement periods

days = number of days in the settlement period

EXAMPLE: Valuing a swap on payment date: Let’s continue our previous example of a one-year, quarterly settlement, $5

million notional swap with a swap fixed rate at initiation of 4.4%. Suppose that after 180 days, the LIBOR term structure is flat

at 3.5% over the next year. Calculate the value of the swap to the fixed-rate receiver.

Because the LIBOR term structure is flat at 3.5%, the new swap fixed rate must be 3.5%.

At t=180, there are two more settlement dates remaining: 90 and 180 days in the future.

EXAMPLE: In a previous example, we determined that the fixed rate on a 1-year quarterly $5,000,000 interest rate swap, given

the following set of spot LIBOR rates, was 1.1% quarterly, or 4.4% on an annual basis.

The current exchange rate is £0.50

The per $. Determine the fixed rate on a

comparable 1-year £ interest rate swap. Then

set of £ determine the notional £ principal

rates are: amount and the quarterly cash

flows on a Pay $ fixed, receive £

fixed currency swap.