Page 302 - P1 Integrated Workbook STUDENT 2018

P. 302

Subject P1: Management Accounting

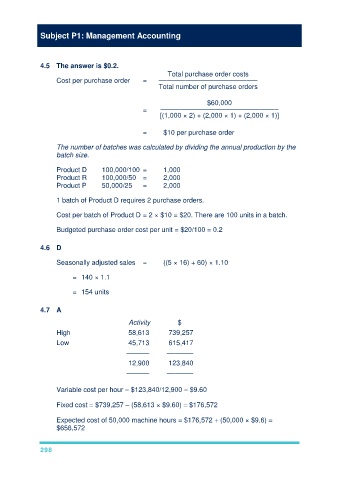

4.5 The answer is $0.2.

Total purchase order costs

Cost per purchase order = ––––––––––––––––––––––––––

Total number of purchase orders

$60,000

= –––––––––––––––––––––––––––––––

[(1,000 × 2) + (2,000 × 1) + (2,000 × 1)]

= $10 per purchase order

The number of batches was calculated by dividing the annual production by the

batch size.

Product D 100,000/100 = 1,000

Product R 100,000/50 = 2,000

Product P 50,000/25 = 2,000

1 batch of Product D requires 2 purchase orders.

Cost per batch of Product D = 2 × $10 = $20. There are 100 units in a batch.

Budgeted purchase order cost per unit = $20/100 = 0.2

4.6 D

Seasonally adjusted sales = ((5 × 16) + 60) × 1.10

= 140 × 1.1

= 154 units

4.7 A

Activity $

High 58,613 739,257

Low 45,713 615,417

–––––– –––––––

12,900 123,840

–––––– –––––––

Variable cost per hour $123,840/12,900 $9.60

Fixed cost $739,257 – (58,613 × $9.60) $176,572

Expected cost of 50,000 machine hours $176,572 (50,000 × $9.6)

$656,572

298