Page 300 - P1 Integrated Workbook STUDENT 2018

P. 300

Subject P1: Management Accounting

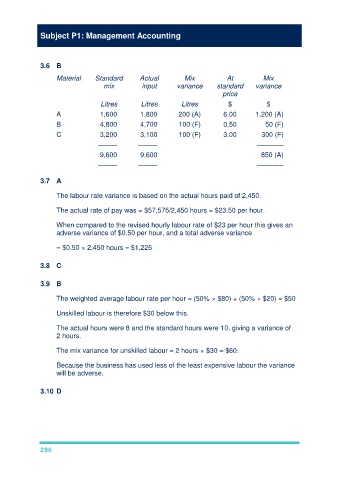

3.6 B

Material Standard Actual Mix At Mix

mix input variance standard variance

price

Litres Litres Litres $ $

A 1,600 1,800 200 (A) 6.00 1,200 (A)

B 4,800 4,700 100 (F) 0.50 50 (F)

C 3,200 3,100 100 (F) 3.00 300 (F)

––––– ––––– –––––––

9,600 9,600 850 (A)

––––– ––––– –––––––

3.7 A

The labour rate variance is based on the actual hours paid of 2,450.

The actual rate of pay was = $57,575/2,450 hours = $23.50 per hour.

When compared to the revised hourly labour rate of $23 per hour this gives an

adverse variance of $0.50 per hour, and a total adverse variance

= $0.50 × 2,450 hours = $1,225

3.8 C

3.9 B

The weighted average labour rate per hour = (50% × $80) + (50% × $20) = $50

Unskilled labour is therefore $30 below this.

The actual hours were 8 and the standard hours were 10, giving a variance of

2 hours.

The mix variance for unskilled labour = 2 hours × $30 = $60.

Because the business has used less of the least expensive labour the variance

will be adverse.

3.10 D

296