Page 14 - FINAL CFA II SLIDES JUNE 2019 DAY 9

P. 14

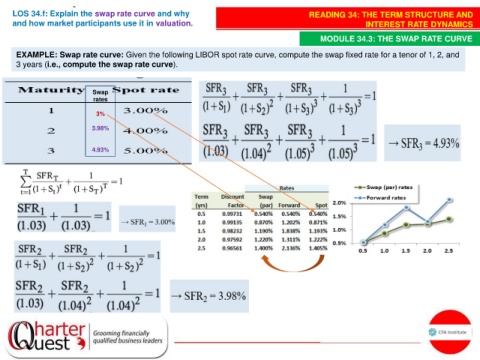

LOS 34.f: Explain the swap rate curve and why READING 34: THE TERM STRUCTURE AND

and how market participants use it in valuation. INTEREST RATE DYNAMICS

MODULE 34.3: THE SWAP RATE CURVE

EXAMPLE: Swap rate curve: Given the following LIBOR spot rate curve, compute the swap fixed rate for a tenor of 1, 2, and

3 years (i.e., compute the swap rate curve).

Swap

rates

3%

3.98%

4.93%