Page 27 - FINAL CFA I SLIDES JUNE 2019 DAY 3

P. 27

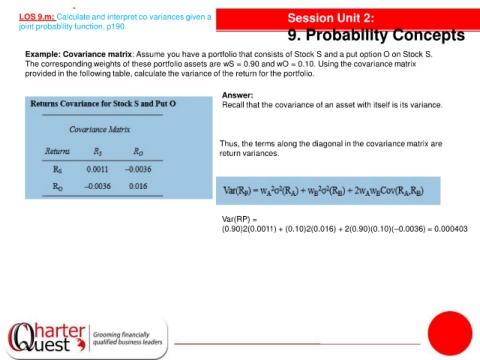

LOS 9.m: Calculate and interpret co variances given a Session Unit 2:

joint probability function, p190.

9. Probability Concepts

Example: Covariance matrix: Assume you have a portfolio that consists of Stock S and a put option O on Stock S.

The corresponding weights of these portfolio assets are wS = 0.90 and wO = 0.10. Using the covariance matrix

provided in the following table, calculate the variance of the return for the portfolio.

Answer:

Recall that the covariance of an asset with itself is its variance.

Thus, the terms along the diagonal in the covariance matrix are

i

return variances.

Var(RP) =

(0.90)2(0.0011) + (0.10)2(0.016) + 2(0.90)(0.10)(–0.0036) = 0.000403