Page 23 - Capital Allowances Recoupments Part 3 (CTA)

P. 23

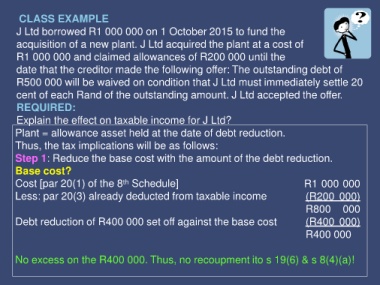

CLASS EXAMPLE

J Ltd borrowed R1 000 000 on 1 October 2015 to fund the

acquisition of a new plant. J Ltd acquired the plant at a cost of

R1 000 000 and claimed allowances of R200 000 until the

date that the creditor made the following offer: The outstanding debt of

R500 000 will be waived on condition that J Ltd must immediately settle 20

cent of each Rand of the outstanding amount. J Ltd accepted the offer.

REQUIRED:

Explain the effect on taxable income for J Ltd?

Plant = allowance asset held at the date of debt reduction.

Thus, the tax implications will be as follows:

Step 1: Reduce the base cost with the amount of the debt reduction.

Base cost?

Cost [par 20(1) of the 8 Schedule] R1 000 000

th

Less: par 20(3) already deducted from taxable income (R200 000)

R800 000

Debt reduction of R400 000 set off against the base cost (R400 000)

R400 000

No excess on the R400 000. Thus, no recoupment ito s 19(6) & s 8(4)(a)!