Page 275 - VIRANSH COACHING CLASSES

P. 275

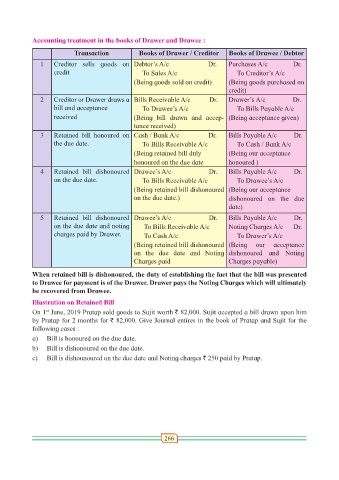

Accounting treatment in the books of Drawer and Drawee :

Transaction Books of Drawer / Creditor Books of Drawee / Debtor

1 Creditor sells goods on Debtor’s A/c Dr. Purchases A/c Dr.

credit To Sales A/c To Creditor’s A/c

(Being goods sold on credit) (Being goods purchased on

credit)

2 Creditor or Drawer draws a Bills Receivable A/c Dr. Drawer’s A/c Dr.

bill and acceptance To Drawee’s A/c To Bills Payable A/c

received (Being bill drawn and accep- (Being acceptance given)

tance received)

3 Retained bill honoured on Cash / Bank A/c Dr. Bills Payable A/c Dr.

the due date. To Bills Receivable A/c To Cash / Bank A/c

(Being retained bill duly (Being our acceptance

honoured on the due date honoured )

4 Retained bill dishonoured Drawee’s A/c Dr. Bills Payable A/c Dr.

on the due date. To Bills Receivable A/c To Drawee’s A/c

(Being retained bill dishonoured (Being our acceptance

on the due date.) dishonoured on the due

date)

5 Retained bill dishonoured Drawee’s A/c Dr. Bills Payable A/c Dr.

on the due date and noting To Bills Receivable A/c Noting Charges A/c Dr.

charges paid by Drawer. To Cash A/c To Drawer’s A/c

(Being retained bill dishonoured (Being our acceptance

on the due date and Noting dishonoured and Noting

Charges paid Charges payable)

When retained bill is dishonoured, the duty of establishing the fact that the bill was presented

to Drawee for payment is of the Drawer. Drawer pays the Noting Charges which will ultimately

be recovered from Drawee.

Illustration on Retained Bill

On 1 June, 2019 Pratap sold goods to Sujit worth ` 82,000. Sujit accepted a bill drawn upon him

st

by Pratap for 2 months for ` 82,000. Give Journal entires in the book of Pratap and Sujit for the

following cases :

a) Bill is honoured on the due date.

b) Bill is dishonoured on the due date.

c) Bill is dishounoured on the due date and Noting charges ` 250 paid by Pratap.

266