Page 164 - ACFE Fraud Reports 2009_2020

P. 164

The Perpetrators

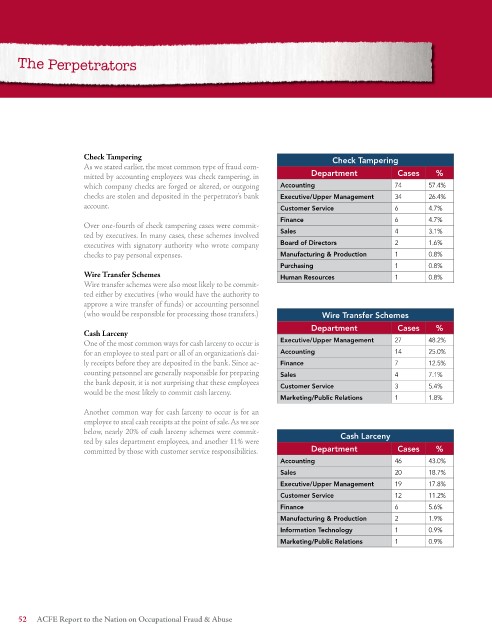

Check Tampering Check Tampering

As we stated earlier, the most common type of fraud com-

mitted by accounting employees was check tampering, in Department Cases %

which company checks are forged or altered, or outgoing Accounting 74 57.4%

checks are stolen and deposited in the perpetrator’s bank Executive/Upper Management 34 26.4%

account. Customer Service 6 4.7%

Finance 6 4.7%

Over one-fourth of check tampering cases were commit-

ted by executives. In many cases, these schemes involved Sales 4 3.1%

executives with signatory authority who wrote company Board of Directors 2 1.6%

checks to pay personal expenses. Manufacturing & Production 1 0.8%

Purchasing 1 0.8%

Wire Transfer Schemes Human Resources 1 0.8%

Wire transfer schemes were also most likely to be commit-

ted either by executives (who would have the authority to

approve a wire transfer of funds) or accounting personnel

(who would be responsible for processing those transfers.) Wire Transfer Schemes

Department Cases %

Cash Larceny

One of the most common ways for cash larceny to occur is Executive/Upper Management 27 48.2%

for an employee to steal part or all of an organization’s dai- Accounting 14 25.0%

ly receipts before they are deposited in the bank. Since ac- Finance 7 12.5%

counting personnel are generally responsible for preparing Sales 4 7.1%

the bank deposit, it is not surprising that these employees Customer Service 3 5.4%

would be the most likely to commit cash larceny.

Marketing/Public Relations 1 1.8%

Another common way for cash larceny to occur is for an

employee to steal cash receipts at the point of sale. As we see

below, nearly 20% of cash larceny schemes were commit- Cash Larceny

ted by sales department employees, and another 11% were

committed by those with customer service responsibilities. Department Cases %

Accounting 46 43.0%

Sales 20 18.7%

Executive/Upper Management 19 17.8%

Customer Service 12 11.2%

Finance 6 5.6%

Manufacturing & Production 2 1.9%

Information Technology 1 0.9%

Marketing/Public Relations 1 0.9%

ACFE Report to the Nation on Occupational Fraud & Abuse