Page 495 - ACFE Fraud Reports 2009_2020

P. 495

How Occupational Fraud Is Committed

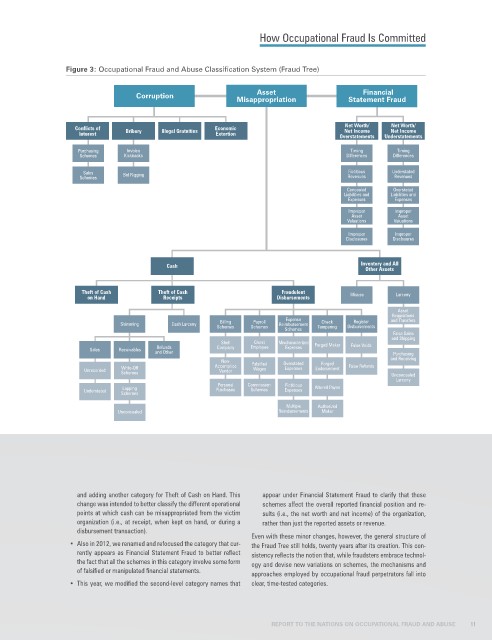

Figure 3: Occupational Fraud and Abuse Classification System (Fraud Tree)

Asset Financial

Corruption

Misappropriation Statement Fraud

Net Worth/ Net Worth/

Conflicts of Economic Net Income Net Income

Interest Bribery Illegal Gratuities Extortion Overstatements Understatements

Purchasing Invoice Timing Timing

Schemes Kickbacks Differences Differences

Sales Fictitious Understated

Schemes Bid Rigging Revenues Revenues

Concealed Overstated

Liabilities and Liabilities and

Expenses Expenses

Improper Improper

Asset Asset

Valuations Valuations

Improper Improper

Disclosures Disclosures

Cash Inventory and All

Other Assets

Theft of Cash Theft of Cash Fraudulent Misuse Larceny

on Hand Receipts Disbursements

Asset

Requisitions

Expense

Skimming Cash Larceny Billing Payroll Reimbursement Check Register and Transfers

Schemes Schemes Schemes Tampering Disbursements

False Sales

and Shipping

Shell Ghost Mischaracterized Forged Maker False Voids

Refunds

Sales Receivables and Other Company Employee Expenses Purchasing

Non- Falsified Overstated Forged and Receiving

Unrecorded Write-Off Accomplice Wages Expenses Endorsement False Refunds Unconcealed

Vendor

Schemes

Larceny

Personal Commission Fictitious Altered Payee

Lapping

Understated Schemes Purchases Schemes Expenses

Multiple Authorized

Unconcealed Reimbursements Maker

and adding another category for Theft of Cash on Hand. This appear under Financial Statement Fraud to clarify that these

change was intended to better classify the different operational schemes affect the overall reported financial position and re-

points at which cash can be misappropriated from the victim sults (i.e., the net worth and net income) of the organization,

organization (i.e., at receipt, when kept on hand, or during a rather than just the reported assets or revenue.

disbursement transaction).

Even with these minor changes, however, the general structure of

• Also in 2012, we renamed and refocused the category that cur- the Fraud Tree still holds, twenty years after its creation. This con-

rently appears as Financial Statement Fraud to better reflect sistency reflects the notion that, while fraudsters embrace technol-

the fact that all the schemes in this category involve some form ogy and devise new variations on schemes, the mechanisms and

of falsified or manipulated financial statements. approaches employed by occupational fraud perpetrators fall into

• This year, we modified the second-level category names that clear, time-tested categories.

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 11