Page 497 - ACFE Fraud Reports 2009_2020

P. 497

How Occupational Fraud Is Committed

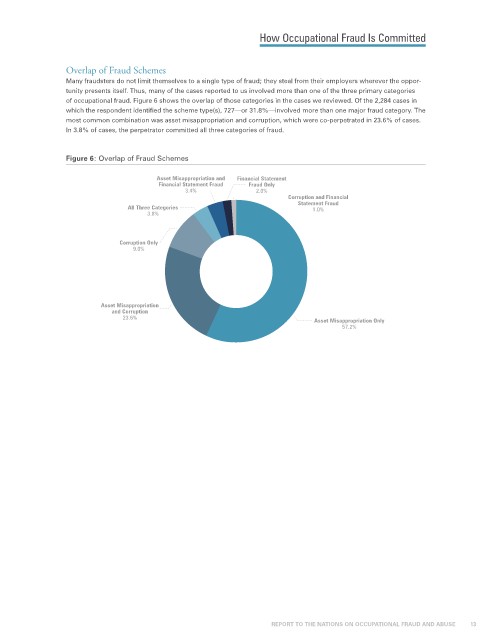

Overlap of Fraud Schemes

Many fraudsters do not limit themselves to a single type of fraud; they steal from their employers wherever the oppor-

tunity presents itself. Thus, many of the cases reported to us involved more than one of the three primary categories

of occupational fraud. Figure 6 shows the overlap of those categories in the cases we reviewed. Of the 2,284 cases in

which the respondent identified the scheme type(s), 727—or 31.8%—involved more than one major fraud category. The

most common combination was asset misappropriation and corruption, which were co-perpetrated in 23.6% of cases.

In 3.8% of cases, the perpetrator committed all three categories of fraud.

Figure 6: Overlap of Fraud Schemes

Asset Misappropriation and Financial Statement

Financial Statement Fraud Fraud Only

3.4% 2.0%

Corruption and Financial

Statement Fraud

All Three Categories 1.0%

3.8%

Corruption Only

9.0%

Asset Misappropriation

and Corruption

23.6% Asset Misappropriation Only

6.6% 2.9% 57.2%

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 13