Page 524 - ACFE Fraud Reports 2009_2020

P. 524

Victim Organizations

Anti-Fraud Controls by Region

Trends in the Implementation of Regional variations in the implemen-

tation rates of anti-fraud controls

Anti-Fraud Controls provide both an interesting perspective

regarding what organizations around

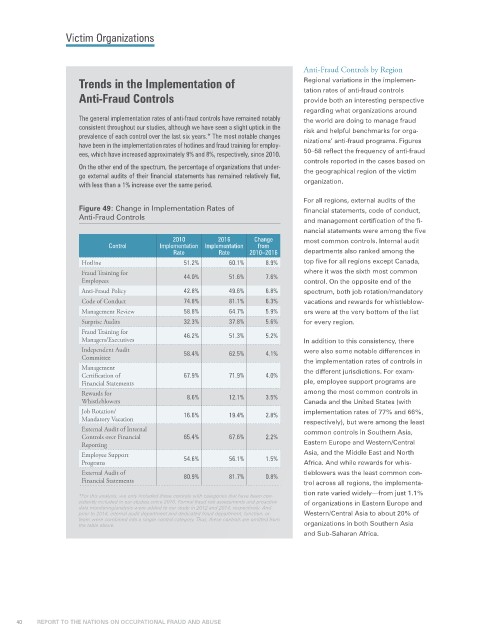

The general implementation rates of anti-fraud controls have remained notably the world are doing to manage fraud

consistent throughout our studies, although we have seen a slight uptick in the risk and helpful benchmarks for orga-

prevalence of each control over the last six years.* The most notable changes

have been in the implementation rates of hotlines and fraud training for employ- nizations’ anti-fraud programs. Figures

ees, which have increased approximately 9% and 8%, respectively, since 2010. 50–58 reflect the frequency of anti-fraud

controls reported in the cases based on

On the other end of the spectrum, the percentage of organizations that under-

go external audits of their financial statements has remained relatively flat, the geographical region of the victim

with less than a 1% increase over the same period. organization.

For all regions, external audits of the

Figure 49: Change in Implementation Rates of financial statements, code of conduct,

Anti-Fraud Controls and management certification of the fi-

nancial statements were among the five

2010 2016 Change most common controls. Internal audit

Control Implementation Implementation from

Rate Rate 2010–2016 departments also ranked among the

Hotline 51.2% 60.1% 8.9% top five for all regions except Canada,

Fraud Training for 44.0% 51.6% 7.6% where it was the sixth most common

Employees control. On the opposite end of the

Anti-Fraud Policy 42.8% 49.6% 6.8% spectrum, both job rotation/mandatory

Code of Conduct 74.8% 81.1% 6.3% vacations and rewards for whistleblow-

Management Review 58.8% 64.7% 5.9% ers were at the very bottom of the list

Surprise Audits 32.3% 37.8% 5.6% for every region.

Fraud Training for 46.2% 51.3% 5.2%

Managers/Executives In addition to this consistency, there

Independent Audit 58.4% 62.5% 4.1% were also some notable differences in

Committee the implementation rates of controls in

Management the different jurisdictions. For exam-

Certification of 67.9% 71.9% 4.0%

Financial Statements ple, employee support programs are

Rewards for 8.6% 12.1% 3.5% among the most common controls in

Whistleblowers Canada and the United States (with

Job Rotation/ 16.6% 19.4% 2.8% implementation rates of 77% and 66%,

Mandatory Vacation respectively), but were among the least

External Audit of Internal common controls in Southern Asia,

Controls over Financial 65.4% 67.6% 2.2%

Reporting Eastern Europe and Western/Central

Employee Support 54.6% 56.1% 1.5% Asia, and the Middle East and North

Programs Africa. And while rewards for whis-

External Audit of 80.9% 81.7% 0.8% tleblowers was the least common con-

Financial Statements trol across all regions, the implementa-

tion rate varied widely—from just 1.1%

*For this analysis, we only included those controls with categories that have been con-

sistently included in our studies since 2010. Formal fraud risk assessments and proactive of organizations in Eastern Europe and

data monitoring/analysis were added to our study in 2012 and 2014, respectively. And

prior to 2014, internal audit department and dedicated fraud department, function, or Western/Central Asia to about 20% of

team were combined into a single control category. Thus, these controls are omitted from

the table above. organizations in both Southern Asia

and Sub-Saharan Africa.

40 REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE