Page 523 - ACFE Fraud Reports 2009_2020

P. 523

Victim Organizations

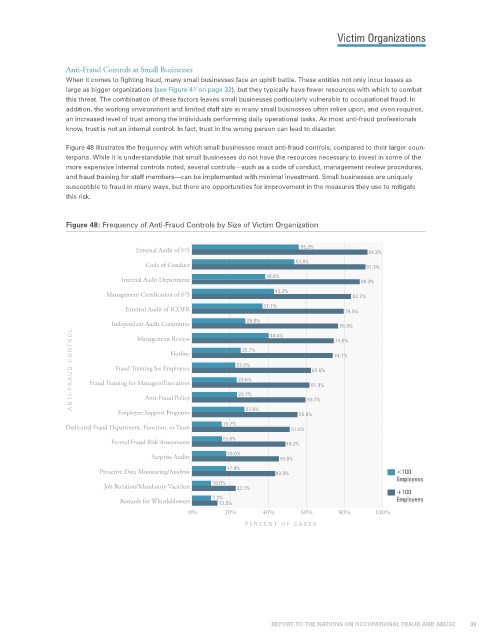

Anti-Fraud Controls at Small Businesses

When it comes to fighting fraud, many small businesses face an uphill battle. These entities not only incur losses as

large as bigger organizations (see Figure 41 on page 32), but they typically have fewer resources with which to combat

this threat. The combination of these factors leaves small businesses particularly vulnerable to occupational fraud. In

addition, the working environment and limited staff size in many small businesses often relies upon, and even requires,

an increased level of trust among the individuals performing daily operational tasks. As most anti-fraud professionals

know, trust is not an internal control. In fact, trust in the wrong person can lead to disaster.

Figure 48 illustrates the frequency with which small businesses enact anti-fraud controls, compared to their larger coun-

terparts. While it is understandable that small businesses do not have the resources necessary to invest in some of the

more expensive internal controls noted, several controls—such as a code of conduct, management review procedures,

and fraud training for staff members—can be implemented with minimal investment. Small businesses are uniquely

susceptible to fraud in many ways, but there are opportunities for improvement in the measures they use to mitigate

this risk.

Figure 48: Frequency of Anti-Fraud Controls by Size of Victim Organization

External Audit of F/S 56.2% 94.2%

Code of Conduct 53.8% 91.3%

Internal Audit Department 38.6% 88.3%

Management Certification of F/S 43.2% 83.7%

External Audit of ICOFR 37.1% 79.9%

Independent Audit Committee 28.0% 40.4% 74.6%

76.9%

ANTI-FRA UD CONTROL Fraud Training for Managers/Executives 22.8% 61.9% 74.1%

Management Review

25.7%

Hotline

Fraud Training for Employees

62.6%

23.6%

Anti-Fraud Policy

59.7%

27.6%

Employee Support Programs 23.7% 55.6%

15.7%

Dedicated Fraud Department, Function, or Team 51.5%

Formal Fraud Risk Assessments 15.8% 49.2%

Surprise Audits 18.0% 45.8%

Proactive Data Monitoring/Analysis 17.9% 43.8% <100

Employees

Job Rotation/Mandatory Vacation 10.0% 23.1%

+100

Rewards for Whistleblowers 7.2% Employees

13.5%

0% 20% 40% 60% 80% 100%

PERCENT OF CASES

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 39