Page 530 - ACFE Fraud Reports 2009_2020

P. 530

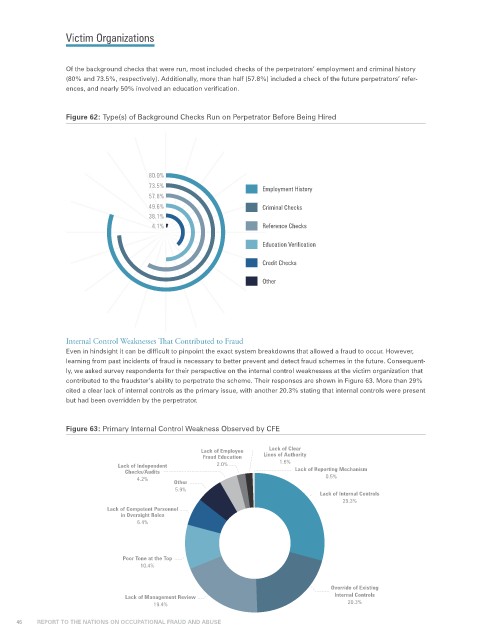

Victim Organizations

Of the background checks that were run, most included checks of the perpetrators’ employment and criminal history

(80% and 73.5%, respectively). Additionally, more than half (57.8%) included a check of the future perpetrators’ refer-

ences, and nearly 50% involved an education verification.

Figure 62: Type(s) of Background Checks Run on Perpetrator Before Being Hired

80.0%

73.5% Employment History

57.8%

49.6% Criminal Checks

38.1%

4.1% Reference Checks

Education Verification

Credit Checks

Other

Internal Control Weaknesses That Contributed to Fraud

Even in hindsight it can be difficult to pinpoint the exact system breakdowns that allowed a fraud to occur. However,

learning from past incidents of fraud is necessary to better prevent and detect fraud schemes in the future. Consequent-

ly, we asked survey respondents for their perspective on the internal control weaknesses at the victim organization that

contributed to the fraudster’s ability to perpetrate the scheme. Their responses are shown in Figure 63. More than 29%

cited a clear lack of internal controls as the primary issue, with another 20.3% stating that internal controls were present

but had been overridden by the perpetrator.

Figure 63: Primary Internal Control Weakness Observed by CFE

Lack of Employee Lack of Clear

Fraud Education Lines of Authority

Lack of Independent 2.0% 1.6%

Checks/Audits Lack of Reporting Mechanism

4.2% 0.5%

Other

5.9%

Lack of Internal Controls

29.3%

Lack of Competent Personnel

in Oversight Roles

6.4%

Poor Tone at the Top

10.4%

Override of Existing

Lack of Management Review 6.6% 2.9% Internal Controls

19.4% 20.3%

46 REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE