Page 540 - ACFE Fraud Reports 2009_2020

P. 540

Perpetrators

Schemes Based on Perpetrator’s Department

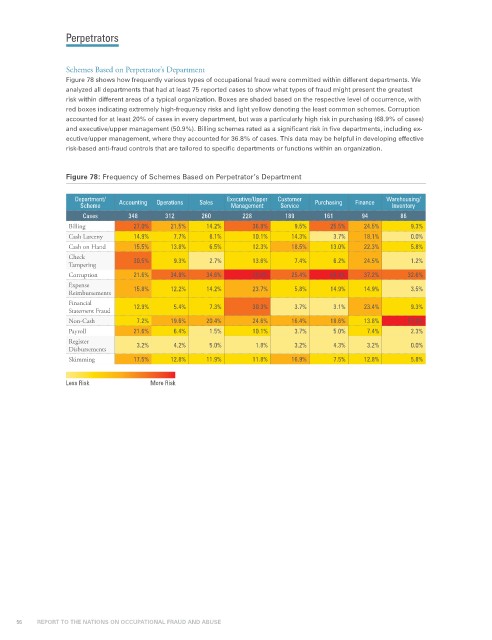

Figure 78 shows how frequently various types of occupational fraud were committed within different departments. We

analyzed all departments that had at least 75 reported cases to show what types of fraud might present the greatest

risk within different areas of a typical organization. Boxes are shaded based on the respective level of occurrence, with

red boxes indicating extremely high-frequency risks and light yellow denoting the least common schemes. Corruption

accounted for at least 20% of cases in every department, but was a particularly high risk in purchasing (68.9% of cases)

and executive/upper management (50.9%). Billing schemes rated as a significant risk in five departments, including ex-

ecutive/upper management, where they accounted for 36.8% of cases. This data may be helpful in developing effective

risk-based anti-fraud controls that are tailored to specific departments or functions within an organization.

Figure 78: Frequency of Schemes Based on Perpetrator’s Department

Department/ Accounting Operations Sales Executive/Upper Customer Purchasing Finance Warehousing/

Scheme Management Service Inventory

Cases 348 312 260 228 189 161 94 86

Billing 27.0% 21.5% 14.2% 36.8% 9.5% 25.5% 24.5% 9.3%

Cash Larceny 14.9% 7.7% 8.1% 10.1% 14.3% 3.7% 18.1% 0.0%

Cash on Hand 15.5% 13.8% 6.5% 12.3% 18.5% 13.0% 22.3% 5.8%

Check 30.5% 9.3% 2.7% 13.6% 7.4% 6.2% 24.5% 1.2%

Tampering

Corruption 21.6% 34.9% 34.6% 50.9% 25.4% 68.9% 37.2% 32.6%

Expense 15.8% 12.2% 14.2% 23.7% 5.8% 14.9% 14.9% 3.5%

Reimbursements

Financial 12.9% 5.4% 7.3% 30.3% 3.7% 3.1% 23.4% 9.3%

Statement Fraud

Non-Cash 7.2% 19.6% 20.4% 24.6% 16.4% 18.6% 13.8% 57.0%

Payroll 21.6% 6.4% 1.5% 10.1% 3.7% 5.0% 7.4% 2.3%

Register 3.2% 4.2% 5.0% 1.8% 3.2% 4.3% 3.2% 0.0%

Disbursements

Skimming 17.5% 12.8% 11.9% 11.8% 16.9% 7.5% 12.8% 5.8%

Less Risk More Risk

56 REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE