Page 594 - ACFE Fraud Reports 2009_2020

P. 594

Median Loss and Duration

by Detection Method

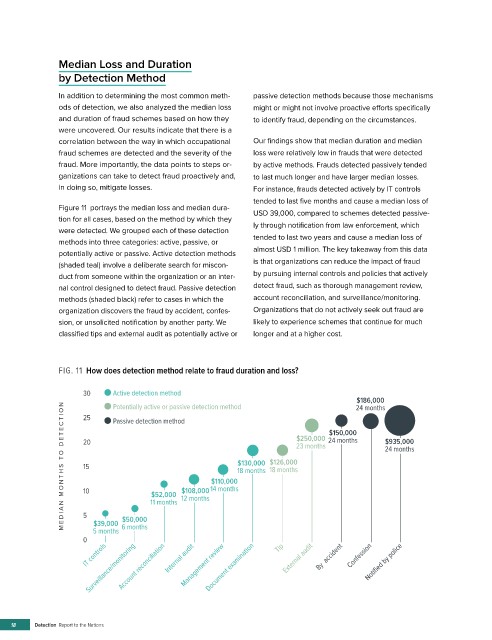

In addition to determining the most common meth- passive detection methods because those mechanisms

ods of detection, we also analyzed the median loss might or might not involve proactive efforts specifically

and duration of fraud schemes based on how they to identify fraud, depending on the circumstances.

were uncovered. Our results indicate that there is a

correlation between the way in which occupational Our findings show that median duration and median

fraud schemes are detected and the severity of the loss were relatively low in frauds that were detected

fraud. More importantly, the data points to steps or- by active methods. Frauds detected passively tended

ganizations can take to detect fraud proactively and, to last much longer and have larger median losses.

in doing so, mitigate losses. For instance, frauds detected actively by IT controls

tended to last five months and cause a median loss of

Figure 11 portrays the median loss and median dura- USD 39,000, compared to schemes detected passive-

tion for all cases, based on the method by which they

were detected. We grouped each of these detection ly through notification from law enforcement, which

methods into three categories: active, passive, or tended to last two years and cause a median loss of

potentially active or passive. Active detection methods almost USD 1 million. The key takeaway from this data

(shaded teal) involve a deliberate search for miscon- is that organizations can reduce the impact of fraud

duct from someone within the organization or an inter- by pursuing internal controls and policies that actively

nal control designed to detect fraud. Passive detection detect fraud, such as thorough management review,

methods (shaded black) refer to cases in which the account reconciliation, and surveillance/monitoring.

organization discovers the fraud by accident, confes- Organizations that do not actively seek out fraud are

sion, or unsolicited notification by another party. We likely to experience schemes that continue for much

classified tips and external audit as potentially active or longer and at a higher cost.

FIG. 11 How does detection method relate to fraud duration and loss?

30 Active detection method

$186,000

Potentially active or passive detection method $150,000 24 months

MEDIAN MONTHS T O DETECTION 20 11 months 12 months 14 months $130,000 18 months $250,000 24 months $935,000

25

Passive detection method

23 months

24 months

$126,000

15

18 months

$110,000

$108,000

10

$52,000

5

$50,000

$39,000

0 5 months 6 months

Surveillance/monitoring Management review

IT controls Internal audit Tip External audit By accident Confession Notified by police

Account reconciliation

Document examination

18 Detection Report to the Nations