Page 593 - ACFE Fraud Reports 2009_2020

P. 593

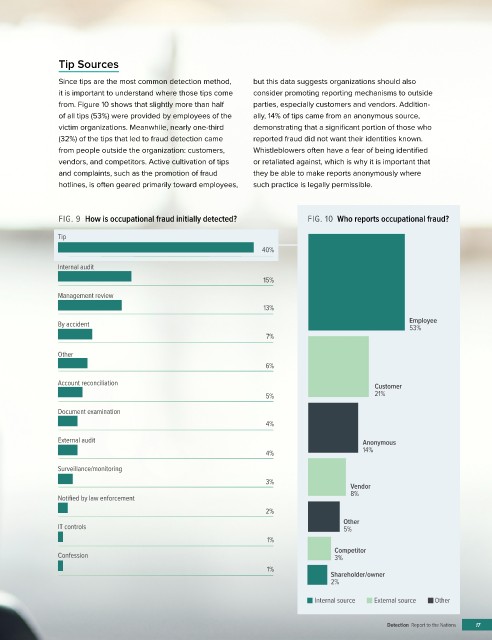

Tip Sources

Since tips are the most common detection method, but this data suggests organizations should also

it is important to understand where those tips come consider promoting reporting mechanisms to outside

from. Figure 10 shows that slightly more than half parties, especially customers and vendors. Addition-

of all tips (53%) were provided by employees of the ally, 14% of tips came from an anonymous source,

victim organizations. Meanwhile, nearly one-third demonstrating that a significant portion of those who

(32%) of the tips that led to fraud detection came reported fraud did not want their identities known.

from people outside the organization: customers, Whistleblowers often have a fear of being identified

vendors, and competitors. Active cultivation of tips or retaliated against, which is why it is important that

and complaints, such as the promotion of fraud they be able to make reports anonymously where

hotlines, is often geared primarily toward employees, such practice is legally permissible.

FIG. 9 How is occupational fraud initially detected? FIG. 10 Who reports occupational fraud?

Tip

40%

Internal audit

15%

Management review

13%

By accident Employee

53%

7%

Other

6%

Account reconciliation Customer

5% 21%

Document examination

4%

External audit Anonymous

4% 14%

Surveillance/monitoring

3%

Vendor

8%

Notified by law enforcement

2%

Other

IT controls 5%

1%

Competitor

Confession 3%

1%

Shareholder/owner

2%

Internal source External source Other

Detection Report to the Nations 17