Page 61 - Agib Bank Ltd Annual Report and IFRS Financial statements 2020

P. 61

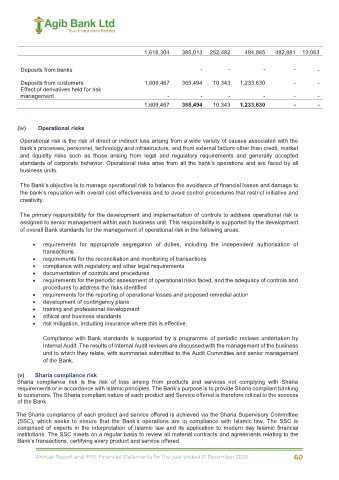

1,618,304 385,013 252,482 484,865 482,881 13,063 The bank is currently holding 558,000 shares in Trust Bank (G) Limited valued at D2.193 million. These shares

were given to the bank by the courts as part settlement of an overdue debt. Annual dividend received does not

Deposits from banks - - - - - form part of the bank’s annual revenue but is rather given out as charity as recommended by the Sharia Board.

We are negotiating with potential buyers to sell it off. Dividend of D0.26 million was received in 2020.

Deposits from customers 1,609,467 365,494 10,343 1,233,630 - -

Effect of derivatives held for risk (vi) Capital management

management - - - - - -

1,609,467 365,494 10,343 1,233,630 - - Regulatory capital

The Central Bank of The Gambia sets and monitors capital requirements for the Bank as a whole. The parent

company and individual banking operations are directly supervised by their local regulators.

(iv) Operational risks

In implementing current capital requirements, The Central Bank of The Gambia requires the bank to maintain a

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associated with the prescribed ratio of total capital to total risk-weighted assets. The bank is also required to maintain a credible

bank’s processes, personnel, technology and infrastructure, and from external factors other than credit, market capital plan to ensure that capital level of the Bank is maintained in consonance with the Bank’s risk appetite.

and liquidity risks such as those arising from legal and regulatory requirements and generally accepted

standards of corporate behavior. Operational risks arise from all the bank’s operations and are faced by all The Bank’s regulatory capital is analysed into two tiers:

business units.

Tier 1 capital, which includes ordinary share capital, share premium, perpetual bonds (which are

The Bank’s objective is to manage operational risk to balance the avoidance of financial losses and damage to classified as innovative Tier 1 securities), retained earnings, translation reserve and other regulatory

the bank’s reputation with overall cost effectiveness and to avoid control procedures that restrict initiative and adjustments relating to items that are included in equity but are treated differently for capital adequacy

creativity. purposes.

The primary responsibility for the development and implementation of controls to address operational risk is Tier 2 capital, which includes qualifying subordinated liabilities, and the element of the fair value

assigned to senior management within each business unit. This responsibility is supported by the development reserve relating to unrealised gains on equity instruments classified as available-for-sale.

of overall Bank standards for the management of operational risk in the following areas:

Various limits are applied to elements of the capital base; qualifying tier 2 capital cannot exceed tier 1 capital;

requirements for appropriate segregation of duties, including the independent authorisation of and qualifying term subordinated loan capital may not exceed 50 percent of tier 1 capital. Other deductions from

transactions capital include the carrying amounts of investments in subsidiaries that are not included in the regulatory

requirements for the reconciliation and monitoring of transactions consolidation, investments in the capital of banks and certain other regulatory items.

compliance with regulatory and other legal requirements

documentation of controls and procedures Banking operations are categorised as either trading book or banking book, and risk-weighted assets are

requirements for the periodic assessment of operational risks faced, and the adequacy of controls and determined according to specified requirements that seek to reflect the varying levels of risk attached to assets

procedures to address the risks identified and off-balance sheet exposures.

requirements for the reporting of operational losses and proposed remedial action

development of contingency plans The bank’s policy is to maintain a strong capital base to maintain investor, creditor and market confidence and to

training and professional development sustain future development of the business. The impact of the level of capital on shareholders’ return is also

ethical and business standards recognised and the Bank recognises the need to maintain a balance between the higher returns that might be

risk mitigation, including insurance where this is effective. possible with greater gearing and the advantages and security afforded by a sound capital position.

Compliance with Bank standards is supported by a programme of periodic reviews undertaken by

Internal Audit. The results of Internal Audit reviews are discussed with the management of the business The bank and its individually regulated operations have complied with all externally imposed capital requirements

throughout the period.

unit to which they relate, with summaries submitted to the Audit Committee and senior management

of the Bank.

There have been no material changes in the bank’s management of capital during the period.

(v) Sharia compliance risk

Sharia compliance risk is the risk of loss arising from products and services not complying with Sharia The Bank’s regulatory capital position at 31 December was as follows:

requirements or in accordance with Islamic principles. The Bank’s purpose is to provide Sharia compliant banking

to customers. The Sharia compliant nature of each product and Service offered is therefore critical to the success % ` 2020 2019

of the Bank. Tier 1 capital

The Sharia compliance of each product and service offered is achieved via the Sharia Supervisory Committee Ordinary share capital 100 241,209 241,209

(SSC), which seeks to ensure that the Bank’s operations are in compliance with Islamic law. The SSC is Share premium 100 2,292 2,292

comprised of experts in the interpretation of Islamic law and its application to modern day Islamic financial Retained earnings 100 (99,059) (115,860)

institutions. The SSC meets on a regular basis to review all material contracts and agreements relating to the 51,942

Bank’s transactions, certifying every product and service offered. Statutory reserves 100 41,228

45 46

Annual Report and IFRS Financial Statements for the year ended 31 December 2020 60