Page 58 - Agib Bank Ltd Annual Report and IFRS Financial statements 2020

P. 58

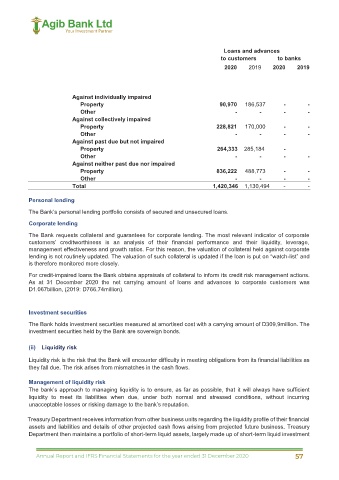

Loans and advances

to customers to banks

2020 2019 2020 2019

Against individually impaired

Property 90,970 186,537 - -

Other - - - -

Against collectively impaired

Property 228,821 170,000 - -

Other - - - -

Against past due but not impaired

Property 264,333 285,184 -

Other - - - -

Against neither past due nor impaired

Property 836,222 488,773 - -

Other - - - -

Total 1,420,346 1,130,494 - -

Personal lending

The Bank’s personal lending portfolio consists of secured and unsecured loans.

Corporate lending

The Bank requests collateral and guarantees for corporate lending. The most relevant indicator of corporate

customers’ creditworthiness is an analysis of their financial performance and their liquidity, leverage,

management effectiveness and growth ratios. For this reason, the valuation of collateral held against corporate

lending is not routinely updated. The valuation of such collateral is updated if the loan is put on “watch-list” and

is therefore monitored more closely.

For credit-impaired loans the Bank obtains appraisals of collateral to inform its credit risk management actions.

As at 31 December 2020 the net carrying amount of loans and advances to corporate customers was

D1.067billion, (2019: D766.74million).

Investment securities

The Bank holds investment securities measured at amortised cost with a carrying amount of D309,9million. The

investment securities held by the Bank are sovereign bonds.

(ii) Liquidity risk

Liquidity risk is the risk that the Bank will encounter difficulty in meeting obligations from its financial liabilities as

they fall due. The risk arises from mismatches in the cash flows.

Management of liquidity risk

The bank’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient

liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring

unacceptable losses or risking damage to the bank’s reputation.

Treasury Department receives information from other business units regarding the liquidity profile of their financial

assets and liabilities and details of other projected cash flows arising from projected future business. Treasury

Department then maintains a portfolio of short-term liquid assets, largely made up of short-term liquid investment

42

Annual Report and IFRS Financial Statements for the year ended 31 December 2020 57