Page 63 - Agib Bank Ltd Annual Report and IFRS Financial statements 2020

P. 63

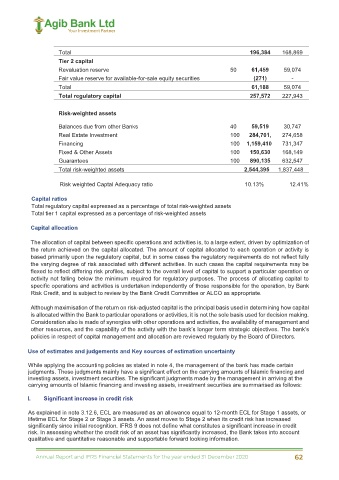

Total 196,384 168,869

Tier 2 capital

Revaluation reserve 50 61,459 59,074

Fair value reserve for available-for-sale equity securities (271) -

Total 61,188 59,074

Total regulatory capital 257,572 227,943

Risk-weighted assets

40

Balances due from other Banks 59,519 30,747

Real Estate Investment 100 284,701, 274,658

Financing 100 1,159,410 731,347

Fixed & Other Assets 100 150,630 168,149

Guarantees 100 890,135 632,547

Total risk-weighted assets 2,544,395 1,837,448

Risk weighted Captal Adequacy ratio 10.13% 12.41%

Capital ratios

Total regulatory capital expressed as a percentage of total risk-weighted assets

Total tier 1 capital expressed as a percentage of risk-weighted assets

Capital allocation

The allocation of capital between specific operations and activities is, to a large extent, driven by optimization of

the return achieved on the capital allocated. The amount of capital allocated to each operation or activity is

based primarily upon the regulatory capital, but in some cases the regulatory requirements do not reflect fully

the varying degree of risk associated with different activities. In such cases the capital requirements may be

flexed to reflect differing risk profiles, subject to the overall level of capital to support a particular operation or

activity not falling below the minimum required for regulatory purposes. The process of allocating capital to

specific operations and activities is undertaken independently of those responsible for the operation, by Bank

Risk Credit, and is subject to review by the Bank Credit Committee or ALCO as appropriate.

Although maximisation of the return on risk-adjusted capital is the principal basis used in determining how capital

is allocated within the Bank to particular operations or activities, it is not the sole basis used for decision making.

Consideration also is made of synergies with other operations and activities, the availability of management and

other resources, and the capability of the activity with the bank’s longer term strategic objectives. The bank’s

policies in respect of capital management and allocation are reviewed regularly by the Board of Directors.

Use of estimates and judgements and Key sources of estimation uncertainty

While applying the accounting policies as stated in note 4, the management of the bank has made certain

judgments. These judgments mainly have a significant effect on the carrying amounts of Islamic financing and

investing assets, investment securities. The significant judgments made by the management in arriving at the

carrying amounts of Islamic financing and investing assets, investment securities are summarised as follows:

I. Significant increase in credit risk

As explained in note 3.12.6, ECL are measured as an allowance equal to 12-month ECL for Stage 1 assets, or

lifetime ECL for Stage 2 or Stage 3 assets. An asset moves to Stage 2 when its credit risk has increased

significantly since initial recognition. IFRS 9 does not define what constitutes a significant increase in credit

risk. In assessing whether the credit risk of an asset has significantly increased, the Bank takes into account

qualitative and quantitative reasonable and supportable forward looking information.

47

Annual Report and IFRS Financial Statements for the year ended 31 December 2020 62