Page 490 - Most-Essential-Learning-Competencies-Matrix-LATEST-EDITION-FROM-BCD

P. 490

490

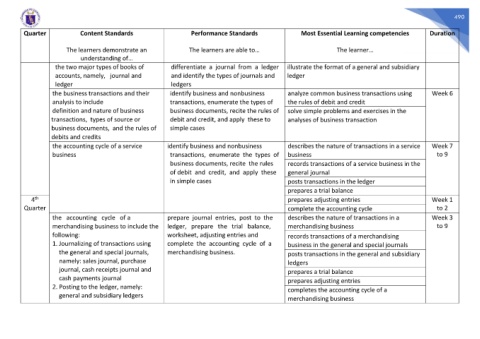

Quarter Content Standards Performance Standards Most Essential Learning competencies Duration

The learners demonstrate an The learners are able to… The learner…

understanding of…

the two major types of books of differentiate a journal from a ledger illustrate the format of a general and subsidiary

accounts, namely, journal and and identify the types of journals and ledger

ledger ledgers

the business transactions and their identify business and nonbusiness analyze common business transactions using Week 6

analysis to include transactions, enumerate the types of the rules of debit and credit

definition and nature of business business documents, recite the rules of solve simple problems and exercises in the

transactions, types of source or debit and credit, and apply these to analyses of business transaction

business documents, and the rules of simple cases

debits and credits

the accounting cycle of a service identify business and nonbusiness describes the nature of transactions in a service Week 7

business transactions, enumerate the types of business to 9

business documents, recite the rules records transactions of a service business in the

of debit and credit, and apply these general journal

in simple cases posts transactions in the ledger

prepares a trial balance

th

4 prepares adjusting entries Week 1

Quarter complete the accounting cycle to 2

the accounting cycle of a prepare journal entries, post to the describes the nature of transactions in a Week 3

merchandising business to include the ledger, prepare the trial balance, merchandising business to 9

following: worksheet, adjusting entries and records transactions of a merchandising

1. Journalizing of transactions using complete the accounting cycle of a business in the general and special journals

the general and special journals, merchandising business. posts transactions in the general and subsidiary

namely: sales journal, purchase ledgers

journal, cash receipts journal and prepares a trial balance

cash payments journal

prepares adjusting entries

2. Posting to the ledger, namely:

completes the accounting cycle of a

general and subsidiary ledgers

merchandising business