Page 167 - IC46 addendum

P. 167

Indian Accounting Standards

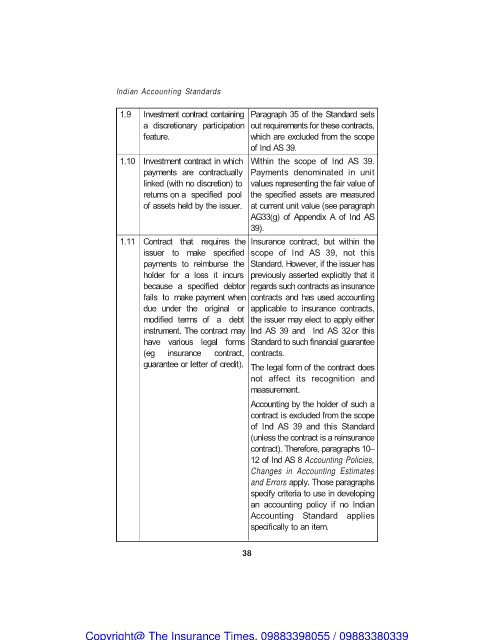

1.9 Investment contract containing Paragraph 35 of the Standard sets

a discretionary participation out requirements for these contracts,

feature. which are excluded from the scope

of Ind AS 39.

1.10 Investment contract in which Within the scope of Ind AS 39.

payments are contractually Payments denominated in unit

linked (with no discretion) to values representing the fair value of

returns on a specified pool the specified assets are measured

of assets held by the issuer. at current unit value (see paragraph

AG33(g) of Appendix A of Ind AS

39).

1.11 Contract that requires the Insurance contract, but within the

issuer to make specified scope of Ind AS 39, not this

payments to reimburse the Standard. However, if the issuer has

holder for a loss it incurs previously asserted explicitly that it

because a specified debtor regards such contracts as insurance

fails to make payment when contracts and has used accounting

due under the original or applicable to insurance contracts,

modified terms of a debt the issuer may elect to apply either

instrument. The contract may Ind AS 39 and Ind AS 32 or this

have various legal forms Standard to such financial guarantee

(eg insurance contract, contracts.

guarantee or letter of credit). The legal form of the contract does

not affect its recognition and

measurement.

Accounting by the holder of such a

contract is excluded from the scope

of Ind AS 39 and this Standard

(unless the contract is a reinsurance

contract). Therefore, paragraphs 10–

12 of Ind AS 8 Accounting Policies,

Changes in Accounting Estimates

and Errors apply. Those paragraphs

specify criteria to use in developing

an accounting policy if no Indian

Accounting Standard applies

specifically to an item.

38

Copyright@ The Insurance Times. 09883398055 / 09883380339