Page 33 - CCFA Journal - Ninth Issue

P. 33

加中金融 风险管理 Risk Management

加中金融

The Stress Testing Framework

压力测试框架

The concept of stress testing was introduced by the Basel

Committee on Banking Supervision (BCBS) in Pillar 2 of Basel 压力测试的概念是由巴塞尔银行监管委员会(BCBS)于

II capital framework in 2005. According to BCBS, “a stress test 2005 年在巴塞尔资本框架的第二支柱中引入的。根据

is commonly described as the evaluation of the financial BCBS 的说法,“压力测试通常被描述为在严峻但合理的

position of a bank under a severe but plausible scenario to 情况下对银行的财务状况进行评估,以帮助银行内部的

assist in decision making within the bank” [1,2]. 决策”[1,2]。

In Canada, the Office of the Superintendent of Financial 在加拿大,加拿大金融机构监管办公室(OSFI) E-18(压力

Institutions Canada (OSFI) E-18 (Stress Testing) required stress 测试)要求银行将压力测试作为健全的商业和金融实践[3]

testing exercises as an integrated component of the sound 的综合组成部分。在 OSFI E-19(存款机构内部资本充足率

business and financial practices [3]. OSFI E-19 (Internal Capital 评估程序(ICAAP))中,明确规定银行在制定资本规划时应

Adequacy Assessment Process (ICAAP) for Deposit-Taking 考虑审慎、前瞻性的压力测试结果,以识别可能的不利

Institutions) emphasized that the rigorous and forward- 事件或市场条件的变化[4]。宏观压力测试(MST)是 OSFI

looking stress testing should be incorporated in the capital 负责制定的对前瞻性宏观经济状况的压力测试情景,银

planning process to identify possible adverse events or 行须向 OSFI 报告在指定压力情景下风险指标表现,包括

changes in market conditions [4]. Macro Stress Test (MST) is 前面提到的信贷风险的 PCL 水平、核心一级资本充足率、

an OSFI prescribed stress scenario on forward looking macro- 流动性覆盖率以及净稳定资金比率。

economic conditions, and banks are required to report a set

of risk measures under this scenario including those 压力测试种类包括情景压力测试和敏感性压力测试,如

mentioned previously such as PCL level for credit risk, CET1 图 1 所示。压力测试情景包括 GDP、CPI、失业率、房价

ratio for regulatory capital and liquidity coverage and net 指数、商品价格、股市波动率、证券收益率差、利率等

stable funding ratio for liquidity risk. 宏观经济和金融指标。压力测试情景评估了全球衰退、

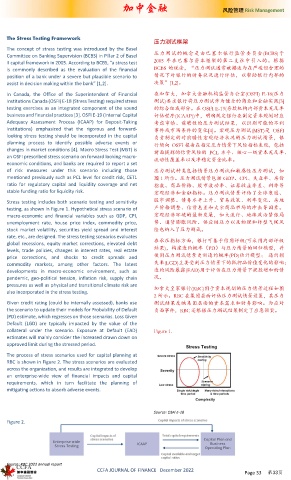

Stress testing includes both scenario testing and sensitivity 股市调整、债务水平上升、贸易政策、利率变化、房地

testing, as shown in Figure 1. Hypothetical stress scenario of 产价格调整、信贷息差和大宗商品市场的冲击等因素。

macro-economic and financial variables such as GDP, CPI, 宏观经济环境的最新发展,如大流行、地缘政治紧张局

unemployment rate, house price index, commodity price, 势、通货膨胀风险、供应链压力以及物理和转型气候风

stock market volatility, securities yield spread and interest 险也纳入了压力测试。

rate, etc., are designed. The stress testing scenarios evaluates

global recessions, equity market corrections, elevated debt 在承压指标方面,银行可基于信用评级(可采用内部评级

levels, trade policies, changes in interest rates, real estate 结果),构建违约概率(PD)与压力情景的回归模型,并

price corrections, and shocks to credit spreads and 使用压力测试情景更新违约概率(PD)估计模型; 违约损

commodity markets, among other factors. The latest 失率(LGD)主要受到压力情景下的抵押品价值变化的影响;

developments in macro-economic environment, such as 违约风险暴露(EAD)用于评估在压力情景下提款增加的情

pandemic, geo-political tension, inflation risk, supply chain 况。

pressures as well as physical and transitional climate risk are 加拿大皇家银行(RBC)用于资本规划的压力情景过程如图

also incorporated in the stress testing.

2 所示。RBC 在集团层面评估压力测试情景设置,其压力

Given credit rating (could be internally assessed), banks use 测试结果反映集团层面的资本需求和财务影响。为应对

the scenario to update their models for Probability of Default 负面事件,RBC 还根据压力测试结果制定了应急预案。

(PD) estimate, which regresses on those scenarios. Loss Given

Default (LGD) are typically impacted by the value of the

collateral under the scenario. Exposure at Default (EAD) Figure 1.

estimates will mainly consider the increased drawn down on

approved limit during the stressed period.

The process of stress scenarios used for capital planning at

RBC is shown in Figure 2. The stress scenarios are evaluated

across the organization, and results are integrated to develop

an enterprise-wide view of financial impacts and capital

requirements, which in turn facilitate the planning of

mitigating actions to absorb adverse events.

Source: OSFI E-18

Figure 2.

Source: RBC 2022 annual report

CCFA JOURNAL OF FINANCE December 2022

Page 33 第33页