Page 49 - P6 Slide - Taxation - Lecture Day 1

P. 49

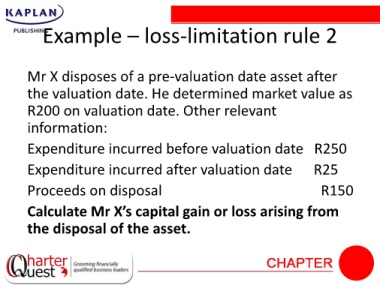

Example – loss-limitation rule 2

Mr X disposes of a pre-valuation date asset after

the valuation date. He determined market value as

R200 on valuation date. Other relevant

information:

Expenditure incurred before valuation date R250

Expenditure incurred after valuation date R25

Proceeds on disposal R150

Calculate Mr X’s capital gain or loss arising from

the disposal of the asset.