Page 443 - ACFE Fraud Reports 2009_2020

P. 443

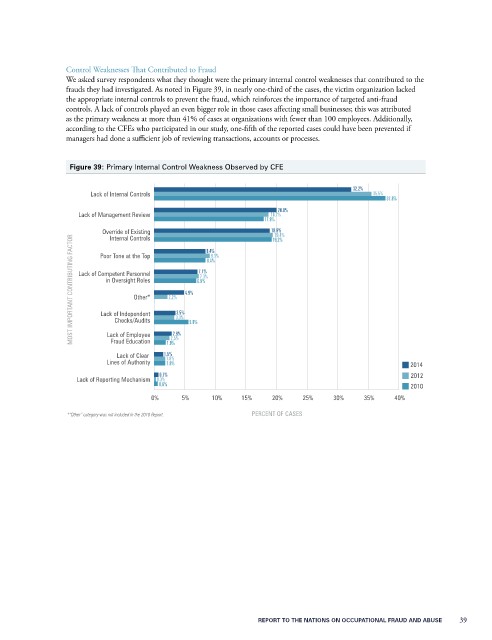

Control Weaknesses That Contributed to Fraud

We asked survey respondents what they thought were the primary internal control weaknesses that contributed to the

frauds they had investigated. As noted in Figure 39, in nearly one-third of the cases, the victim organization lacked

the appropriate internal controls to prevent the fraud, which reinforces the importance of targeted anti-fraud

controls. A lack of controls played an even bigger role in those cases affecting small businesses; this was attributed

as the primary weakness at more than 41% of cases at organizations with fewer than 100 employees. Additionally,

according to the CFEs who participated in our study, one-fifth of the reported cases could have been prevented if

managers had done a sufficient job of reviewing transactions, accounts or processes.

Figure 39: Primary Internal Control Weakness Observed by CFE

32.2%

Lack of Internal Controls 35.5%

37.8%

20.0%

Lack of Management Review 18.7%

17.9%

Override of Existing 8.4% 18.9%

19.4%

Internal Controls

MOST IMPORTANT CONTRIBUTING FACTOR Lack of Competent Personnel 2.2% 3.3% 4.9% 6.9%

19.2%

Poor Tone at the Top

9.1%

8.4%

7.1%

7.3%

in Oversight Roles

Other*

3.5%

Lack of Independent

Checks/Audits

5.6%

2.9%

Lack of Employee

Fraud Education

1.9%

Lack of Clear 1.5% 2.5%

Lines of Authority 1.8% 2014

1.8%

0.7% 2012

Lack of Reporting Mechanism 0.3%

0.6% 2010

0% 5% 10% 15% 20% 25% 30% 35% 40%

*“Other” category was not included in the 2010 Report. PERCENT OF CASES

RepoRt to the NatioNs oN occupatioNal FRaud aNd abuse 39