Page 22 - PowerPoint Presentation

P. 22

LOS 34.k: Describe modern term structure READING 34: THE TERM STRUCTURE AND

models and how they are used. INTEREST RATE DYNAMICS

MODULE 34.6: INTEREST RATE MODELS

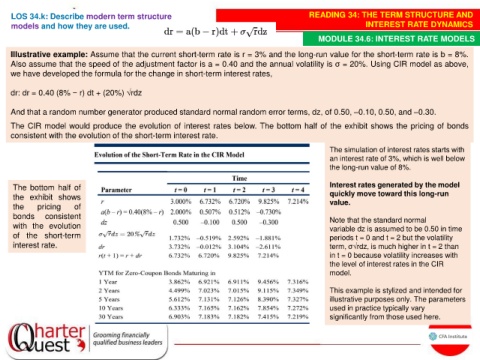

Illustrative example: Assume that the current short-term rate is r = 3% and the long-run value for the short-term rate is b = 8%.

Also assume that the speed of the adjustment factor is a = 0.40 and the annual volatility is σ = 20%. Using CIR model as above,

we have developed the formula for the change in short-term interest rates,

dr: dr = 0.40 (8% − r) dt + (20%) √rdz

And that a random number generator produced standard normal random error terms, dz, of 0.50, –0.10, 0.50, and –0.30.

The CIR model would produce the evolution of interest rates below. The bottom half of the exhibit shows the pricing of bonds

consistent with the evolution of the short-term interest rate.

The simulation of interest rates starts with

an interest rate of 3%, which is well below

the long-run value of 8%.

The bottom half of Interest rates generated by the model

the exhibit shows quickly move toward this long-run

value.

the pricing of

bonds consistent Note that the standard normal

with the evolution variable dz is assumed to be 0.50 in time

of the short-term periods t = 0 and t = 2 but the volatility

interest rate. term, σ√rdz, is much higher in t = 2 than

in t = 0 because volatility increases with

the level of interest rates in the CIR

model.

This example is stylized and intended for

illustrative purposes only. The parameters

used in practice typically vary

significantly from those used here.