Page 21 - PowerPoint Presentation

P. 21

LOS 34.k: Describe modern term structure READING 34: THE TERM STRUCTURE AND

models and how they are used. INTEREST RATE DYNAMICS

MODULE 34.6: INTEREST RATE MODELS

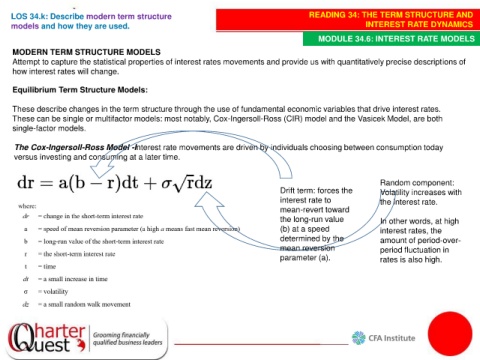

MODERN TERM STRUCTURE MODELS

Attempt to capture the statistical properties of interest rates movements and provide us with quantitatively precise descriptions of

how interest rates will change.

Equilibrium Term Structure Models:

These describe changes in the term structure through the use of fundamental economic variables that drive interest rates.

These can be single or multifactor models: most notably, Cox-Ingersoll-Ross (CIR) model and the Vasicek Model, are both

single-factor models.

The Cox-Ingersoll-Ross Model -Interest rate movements are driven by individuals choosing between consumption today

versus investing and consuming at a later time.

Random component:

Drift term: forces the Volatility increases with

interest rate to the interest rate.

mean-revert toward

the long-run value In other words, at high

(b) at a speed interest rates, the

determined by the amount of period-over-

mean reversion period fluctuation in

parameter (a). rates is also high.