Page 48 - PowerPoint Presentation

P. 48

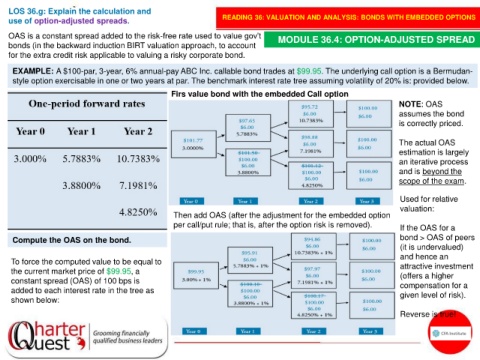

LOS 36.g: Explain the calculation and

use of option-adjusted spreads. READING 36: VALUATION AND ANALYSIS: BONDS WITH EMBEDDED OPTIONS

OAS is a constant spread added to the risk-free rate used to value gov’t MODULE 36.4: OPTION-ADJUSTED SPREAD

bonds (in the backward induction BIRT valuation approach, to account

for the extra credit risk applicable to valuing a risky corporate bond.

EXAMPLE: A $100-par, 3-year, 6% annual-pay ABC Inc. callable bond trades at $99.95. The underlying call option is a Bermudan-

style option exercisable in one or two years at par. The benchmark interest rate tree assuming volatility of 20% is: provided below.

Firs value bond with the embedded Call option

NOTE: OAS

assumes the bond

is correctly priced.

The actual OAS

estimation is largely

an iterative process

and is beyond the

scope of the exam.

Used for relative

valuation:

Then add OAS (after the adjustment for the embedded option

per call/put rule; that is, after the option risk is removed). If the OAS for a

Compute the OAS on the bond. bond > OAS of peers

(it is undervalued)

and hence an

To force the computed value to be equal to attractive investment

the current market price of $99.95, a (offers a higher

constant spread (OAS) of 100 bps is compensation for a

added to each interest rate in the tree as given level of risk).

shown below:

Reverse is true!