Page 52 - PowerPoint Presentation

P. 52

LOS 36.k: Describe the use of one-sided durations READING 36: VALUATION AND ANALYSIS: BONDS WITH EMBEDDED OPTIONS

and key rate durations to evaluate the interest rate

sensitivity of bonds with embedded options.

MODULE 36.6: KEY RATE DURATION

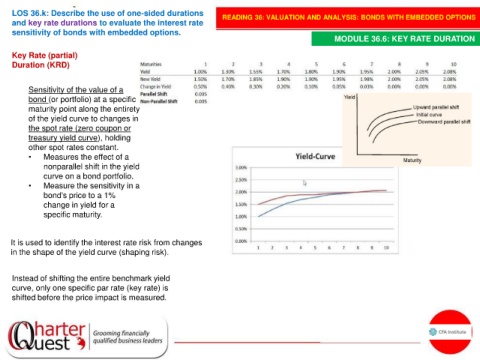

Key Rate (partial)

Duration (KRD)

Sensitivity of the value of a

bond (or portfolio) at a specific

maturity point along the entirety

of the yield curve to changes in

the spot rate (zero coupon or

treasury yield curve), holding

other spot rates constant.

• Measures the effect of a

nonparallel shift in the yield

curve on a bond portfolio.

• Measure the sensitivity in a

bond's price to a 1%

change in yield for a

specific maturity.

It is used to identify the interest rate risk from changes

in the shape of the yield curve (shaping risk).

Instead of shifting the entire benchmark yield

curve, only one specific par rate (key rate) is

shifted before the price impact is measured.