Page 50 - PowerPoint Presentation

P. 50

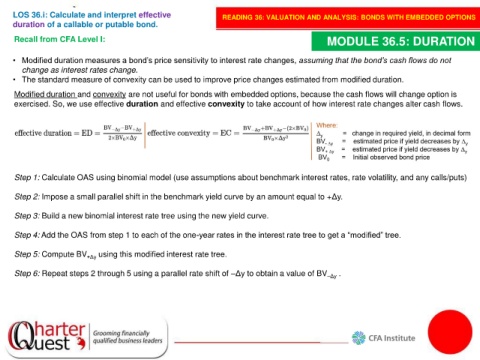

LOS 36.i: Calculate and interpret effective READING 36: VALUATION AND ANALYSIS: BONDS WITH EMBEDDED OPTIONS

duration of a callable or putable bond.

Recall from CFA Level I: MODULE 36.5: DURATION

• Modified duration measures a bond’s price sensitivity to interest rate changes, assuming that the bond’s cash flows do not

change as interest rates change.

• The standard measure of convexity can be used to improve price changes estimated from modified duration.

Modified duration and convexity are not useful for bonds with embedded options, because the cash flows will change option is

exercised. So, we use effective duration and effective convexity to take account of how interest rate changes alter cash flows.

Step 1: Calculate OAS using binomial model (use assumptions about benchmark interest rates, rate volatility, and any calls/puts)

Step 2: Impose a small parallel shift in the benchmark yield curve by an amount equal to +Δy.

Step 3: Build a new binomial interest rate tree using the new yield curve.

Step 4: Add the OAS from step 1 to each of the one-year rates in the interest rate tree to get a “modified” tree.

Step 5: Compute BV +Δy using this modified interest rate tree.

Step 6: Repeat steps 2 through 5 using a parallel rate shift of –Δy to obtain a value of BV –Δy .