Page 53 - PowerPoint Presentation

P. 53

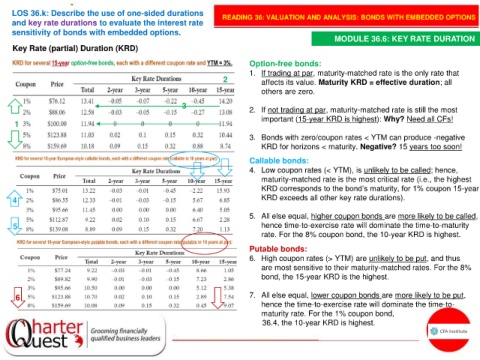

LOS 36.k: Describe the use of one-sided durations READING 36: VALUATION AND ANALYSIS: BONDS WITH EMBEDDED OPTIONS

and key rate durations to evaluate the interest rate

sensitivity of bonds with embedded options.

MODULE 36.6: KEY RATE DURATION

Key Rate (partial) Duration (KRD)

Option-free bonds:

1. If trading at par, maturity-matched rate is the only rate that

2 affects its value. Maturity KRD = effective duration; all

others are zero.

3

2. If not trading at par, maturity-matched rate is still the most

important (15-year KRD is highest): Why? Need all CFs!

1

3. Bonds with zero/coupon rates < YTM can produce -negative

KRD for horizons < maturity. Negative? 15 years too soon!

Callable bonds:

4. Low coupon rates (< YTM), is unlikely to be called; hence,

maturity-matched rate is the most critical rate (i.e., the highest

KRD corresponds to the bond’s maturity, for 1% coupon 15-year

4 KRD exceeds all other key rate durations).

5. All else equal, higher coupon bonds are more likely to be called,

5 hence time-to-exercise rate will dominate the time-to-maturity

rate. For the 8% coupon bond, the 10-year KRD is highest.

Putable bonds:

6. High coupon rates (> YTM) are unlikely to be put, and thus

are most sensitive to their maturity-matched rates. For the 8%

bond, the 15-year KRD is the highest.

6 7. All else equal, lower coupon bonds are more likely to be put,

hence the time-to-exercise rate will dominate the time-to-

maturity rate. For the 1% coupon bond,

36.4, the 10-year KRD is highest.