Page 54 - PowerPoint Presentation

P. 54

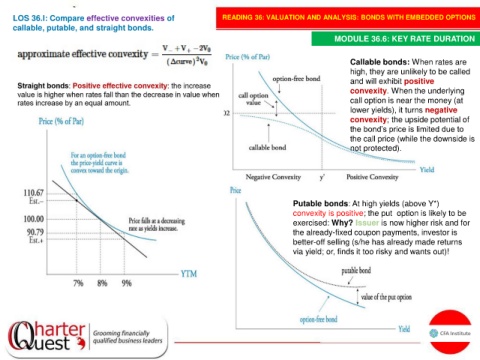

LOS 36.l: Compare effective convexities of READING 36: VALUATION AND ANALYSIS: BONDS WITH EMBEDDED OPTIONS

callable, putable, and straight bonds.

MODULE 36.6: KEY RATE DURATION

Callable bonds: When rates are

high, they are unlikely to be called

and will exhibit positive

convexity. When the underlying

call option is near the money (at

lower yields), it turns negative

convexity; the upside potential of

the bond’s price is limited due to

the call price (while the downside is

not protected).

Putable bonds: At high yields (above Y*)

convexity is positive; the put option is likely to be

exercised: Why? Issuer is now higher risk and for

the already-fixed coupon payments, investor is

better-off selling (s/he has already made returns

via yield; or, finds it too risky and wants out)!