Page 91 - Internal Auditing Standards

P. 91

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

7.5 Materiality Levels

Paragraph # Relevant Extracts from ISAs

320.12 The auditor shall revise materiality for the financial statements as a whole (and, if applicable,

the materiality level or levels for particular classes of transactions, account balances or

disclosures) in the event of becoming aware of information during the audit that would have

caused the auditor to have determined a different amount (or amounts) initially. (Ref: Para. A13)

320.13 If the auditor concludes that a lower materiality for the financial statements as a whole (and, if

applicable, materiality level or levels for particular classes of transactions, account balances or

disclosures) than that initially determined is appropriate, the auditor shall determine whether

it is necessary to revise performance materiality, and whether the nature, timing and extent of

the further audit procedures remain appropriate.

320.14 The auditor shall include in the audit documentation the following amounts and the factors

considered in their determination:

(a) Materiality for the financial statements as a whole;

(b) If applicable, the materiality level or levels for particular classes of transactions, account

balances or disclosures;

(c) Performance materiality; and

(d) Any revision of (a)-(c) as the audit progressed.

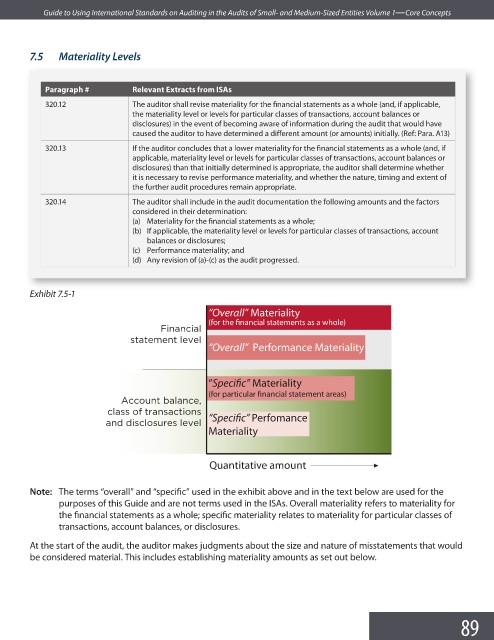

Exhibit 7.5-1

“Overall” Materiality

(for the financial statements as a whole)

4W\O\QWOZ

abObS[S\b ZSdSZ

“Overall” Performance Materiality

“Speci c” Materiality

(for particular financial statement areas)

/QQ]c\b POZO\QS

QZOaa ]T b`O\aOQbW]\a

O\R RWaQZ]ac`Sa ZSdSZ “Speci c” Perfomance

Materiality

Quantitative amount

Note: The terms “overall” and “specific” used in the exhibit above and in the text below are used for the

purposes of this Guide and are not terms used in the ISAs. Overall materiality refers to materiality for

the financial statements as a whole; specific materiality relates to materiality for particular classes of

transactions, account balances, or disclosures.

At the start of the audit, the auditor makes judgments about the size and nature of misstatements that would

be considered material. This includes establishing materiality amounts as set out below.

89