Page 501 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 501

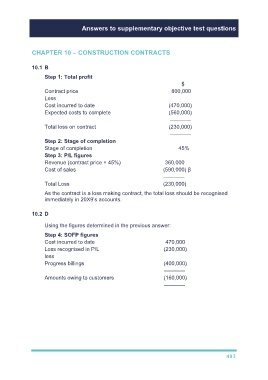

Answers to supplementary objective test questions

CHAPTER 10 – CONSTRUCTION CONTRACTS

10.1 B

Step 1: Total profit

$

Contract price 800,000

Less

Cost incurred to date (470,000)

Expected costs to complete (560,000)

–––––––

Total loss on contract (230,000)

–––––––

Step 2: Stage of completion

Stage of completion 45%

Step 3: P/L figures

Revenue (contract price × 45%) 360,000

Cost of sales (590,000) β

–––––––

Total Loss (230,000)

As the contract is a loss making contract, the total loss should be recognised

immediately in 20X9’s accounts.

10.2 D

Using the figures determined in the previous answer:

Step 4: SOFP figures

Cost incurred to date 470,000

Loss recognised in P/L (230,000)

less

Progress billings (400,000)

–––––––

Amounts owing to customers (160,000)

–––––––

493