Page 31 - PowerPoint Presentation

P. 31

LOS 34.m: Explain the maturity structure of yield READING 34: THE TERM STRUCTURE AND

volatilities and their effect on price volatility. INTEREST RATE DYNAMICS

MODULE 34.5: TERM STRUCTURE THEORY

The term structure of interest rate volatility is the graph of yield volatility versus maturity. It is important because interest

rate volatility is a key concern for bond managers because interest rate volatility drives price volatility in a fixed income

portfolio, especially when securities have embedded options, which are especially sensitive to volatility.

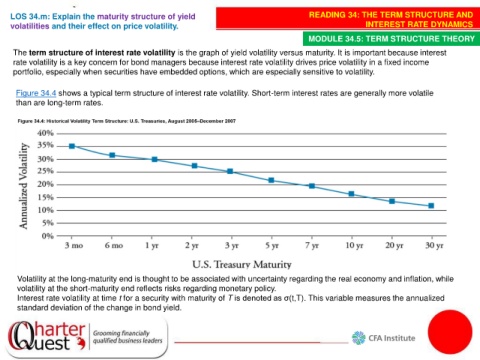

Figure 34.4 shows a typical term structure of interest rate volatility. Short-term interest rates are generally more volatile

than are long-term rates.

Volatility at the long-maturity end is thought to be associated with uncertainty regarding the real economy and inflation, while

volatility at the short-maturity end reflects risks regarding monetary policy.

Interest rate volatility at time t for a security with maturity of T is denoted as σ(t,T). This variable measures the annualized

standard deviation of the change in bond yield.