Page 17 - P6 Slide Taxation - Lecture Day 7 - Various Topics

P. 17

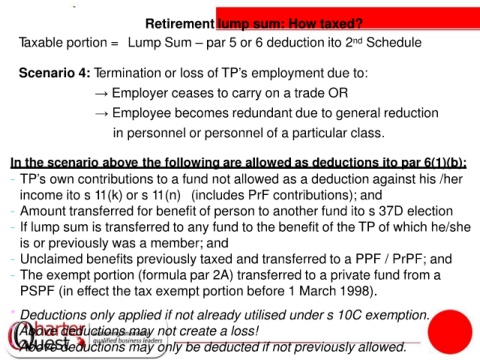

Retirement lump sum: How taxed?

• Taxable portion = Lump Sum – par 5 or 6 deduction ito 2 Schedule

nd

• Scenario 4: Termination or loss of TP’s employment due to:

→ Employer ceases to carry on a trade OR

→ Employee becomes redundant due to general reduction

in personnel or personnel of a particular class.

In the scenario above the following are allowed as deductions ito par 6(1)(b):

- TP’s own contributions to a fund not allowed as a deduction against his /her

income ito s 11(k) or s 11(n) (includes PrF contributions); and

- Amount transferred for benefit of person to another fund ito s 37D election

- If lump sum is transferred to any fund to the benefit of the TP of which he/she

is or previously was a member; and

- Unclaimed benefits previously taxed and transferred to a PPF / PrPF; and

- The exempt portion (formula par 2A) transferred to a private fund from a

PSPF (in effect the tax exempt portion before 1 March 1998).

* Deductions only applied if not already utilised under s 10C exemption.

* Above deductions may not create a loss!

* Above deductions may only be deducted if not previously allowed.