Page 10 - FINAL CFA II SLIDES JUNE 2019 DAY 7

P. 10

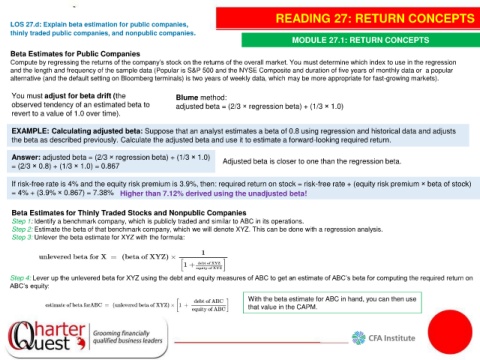

READING 27: RETURN CONCEPTS

LOS 27.d: Explain beta estimation for public companies,

thinly traded public companies, and nonpublic companies.

MODULE 27.1: RETURN CONCEPTS

Beta Estimates for Public Companies

Compute by regressing the returns of the company’s stock on the returns of the overall market. You must determine which index to use in the regression

and the length and frequency of the sample data (Popular is S&P 500 and the NYSE Composite and duration of five years of monthly data or a popular

alternative (and the default setting on Bloomberg terminals) is two years of weekly data, which may be more appropriate for fast-growing markets).

You must adjust for beta drift (the Blume method:

observed tendency of an estimated beta to adjusted beta = (2/3 × regression beta) + (1/3 × 1.0)

revert to a value of 1.0 over time).

EXAMPLE: Calculating adjusted beta: Suppose that an analyst estimates a beta of 0.8 using regression and historical data and adjusts

the beta as described previously. Calculate the adjusted beta and use it to estimate a forward-looking required return.

Answer: adjusted beta = (2/3 × regression beta) + (1/3 × 1.0) Adjusted beta is closer to one than the regression beta.

= (2/3 × 0.8) + (1/3 × 1.0) = 0.867

If risk-free rate is 4% and the equity risk premium is 3.9%, then: required return on stock = risk-free rate + (equity risk premium × beta of stock)

= 4% + (3.9% × 0.867) = 7.38% Higher than 7.12% derived using the unadjusted beta!

Beta Estimates for Thinly Traded Stocks and Nonpublic Companies

Step 1: Identify a benchmark company, which is publicly traded and similar to ABC in its operations.

Step 2: Estimate the beta of that benchmark company, which we will denote XYZ. This can be done with a regression analysis.

Step 3: Unlever the beta estimate for XYZ with the formula:

Step 4: Lever up the unlevered beta for XYZ using the debt and equity measures of ABC to get an estimate of ABC’s beta for computing the required return on

ABC’s equity:

With the beta estimate for ABC in hand, you can then use

that value in the CAPM.